Graphing Digital Assets

Month in Review — February 2026

Bitcoin markets experienced a sharp drawdown in early February, with prices declining rapidly over several sessions as risk assets broadly weakened. While macro sentiment and general risk reduction contributed to the move, the speed and intensity of the selloff raised questions about whether market structure itself amplified the decline.

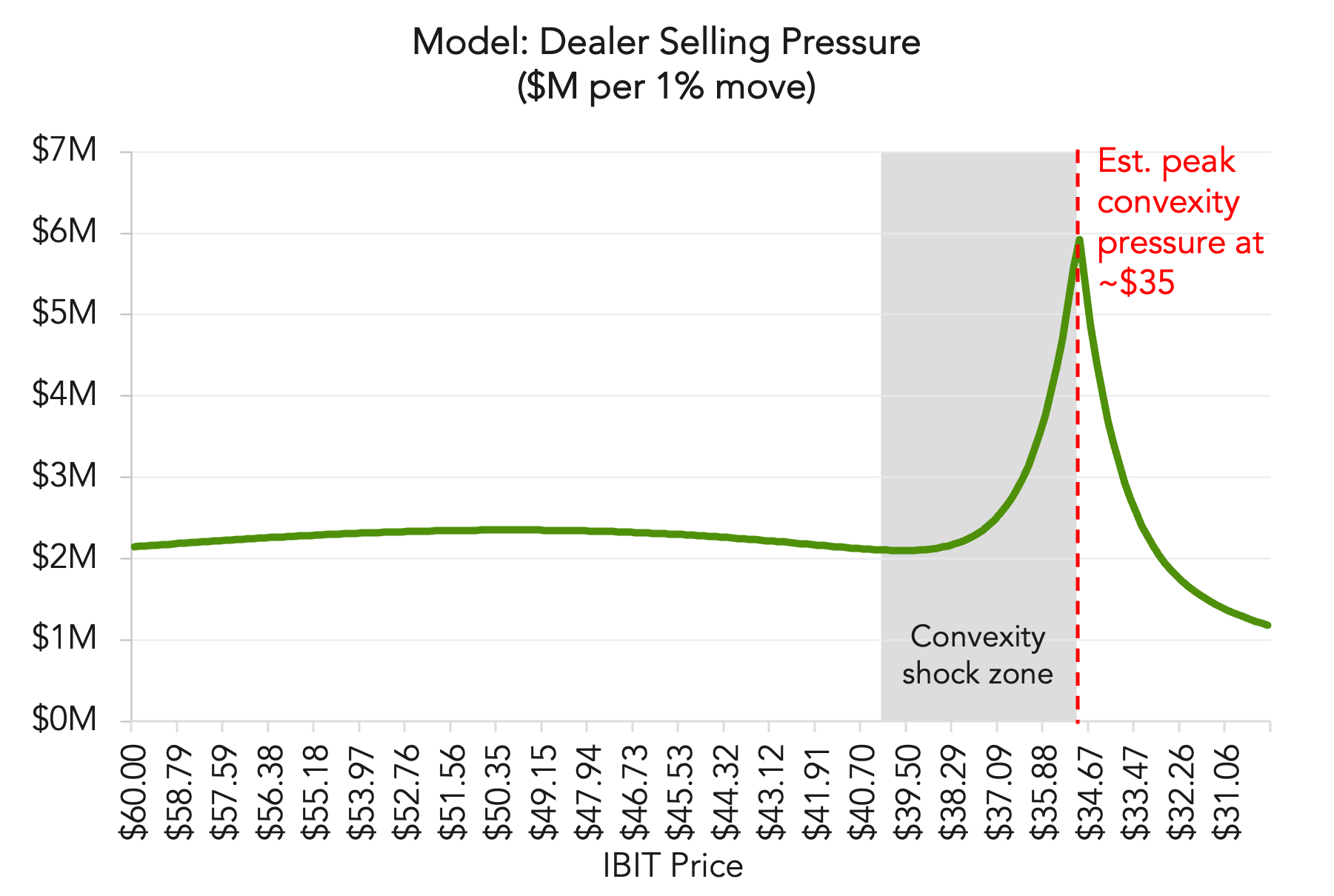

In a recent analysis, we examined how structured products linked to BlackRock’s IBIT ETF introduced convexity into digital asset markets. Many structured notes referencing IBIT embed barrier features that require dealers to dynamically hedge their exposure. As prices decline toward these trigger levels, dealers may need to sell additional exposure to remain hedged, creating a feedback loop that can accelerate price moves.

Our model estimates that this dynamic becomes increasingly pronounced as IBIT approaches key downside thresholds. As illustrated in Figure 1, dealer hedging pressure rises sharply in what we describe as a potential “convexity shock zone” where prices approach $35. Once these levels are reached, relatively small price moves can trigger disproportionately large hedging flows.

Price and flow data during February were broadly consistent with this framework. As shown in Figure 2, the largest IBIT outflows occurred during the initial phase of the selloff, coinciding with a rapid decline in price. Notably, even as flows later stabilized and turned positive toward month-end, prices remained volatile, suggesting that hedging flows and positioning effects continued to influence market behavior throughout February.

These dynamics reflect a broader shift in digital asset markets. As institutional participation expands, price behavior is increasingly shaped by ETF flows, derivatives positioning, and structured products, introducing forms of convexity more commonly observed in traditional financial markets.

For a deeper breakdown of the mechanics behind the early February selloff and a detailed explanation of the dealer selling pressure model, read our full analysis here.

When Convexity Dominates Market Structure

Figure 1

Source: Samara Alpha Management. See article Addendum for model assumptions.

Note: This is a simplified, continuous-time heuristic model designed to visualize aggregate structural convexity. Real-world dealer flows are highly path-dependent and subject to discrete trading frictions, shifts in the volatility surface, and the specific term structures of individual autocallable notes.

Figure 2

As of February 28, 2026. Source for IBIT net flows: https://www.theblock.co/data/etfs/bitcoin-etf/blackrock-ibit-flows; source for IBIT daily close price is Yahoo Finance.

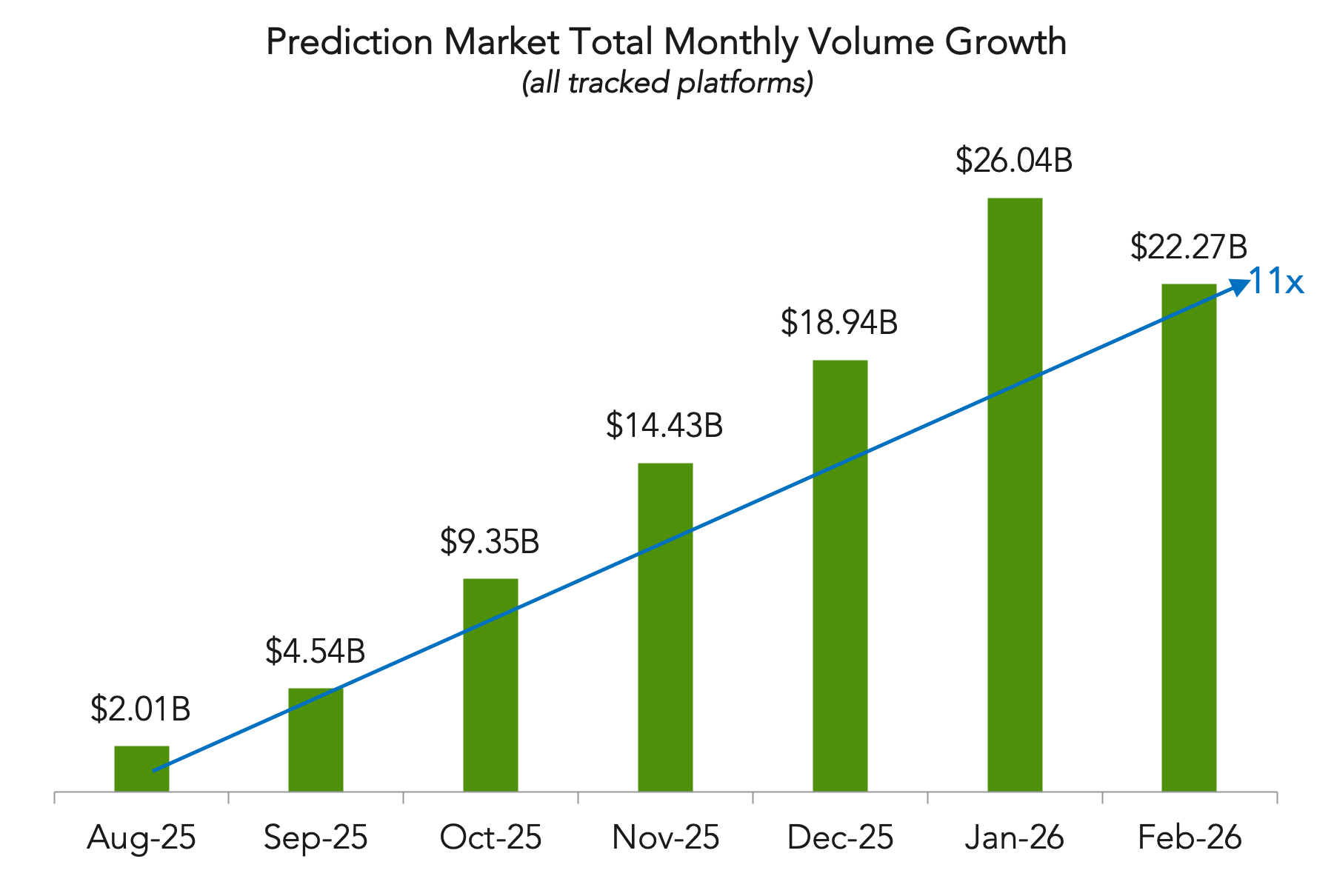

Prediction markets have experienced explosive growth over the past year, emerging as a new venue for pricing uncertainty around real-world events. Platforms such as Polymarket, which operates on blockchain infrastructure and settles trades using stablecoins and smart contracts, and Kalshi, a CFTC-regulated derivatives exchange, allow participants to trade probabilities on outcomes ranging from elections to geopolitical developments. In this structure, the tradable instrument is not a financial asset, but the probability of an event itself.

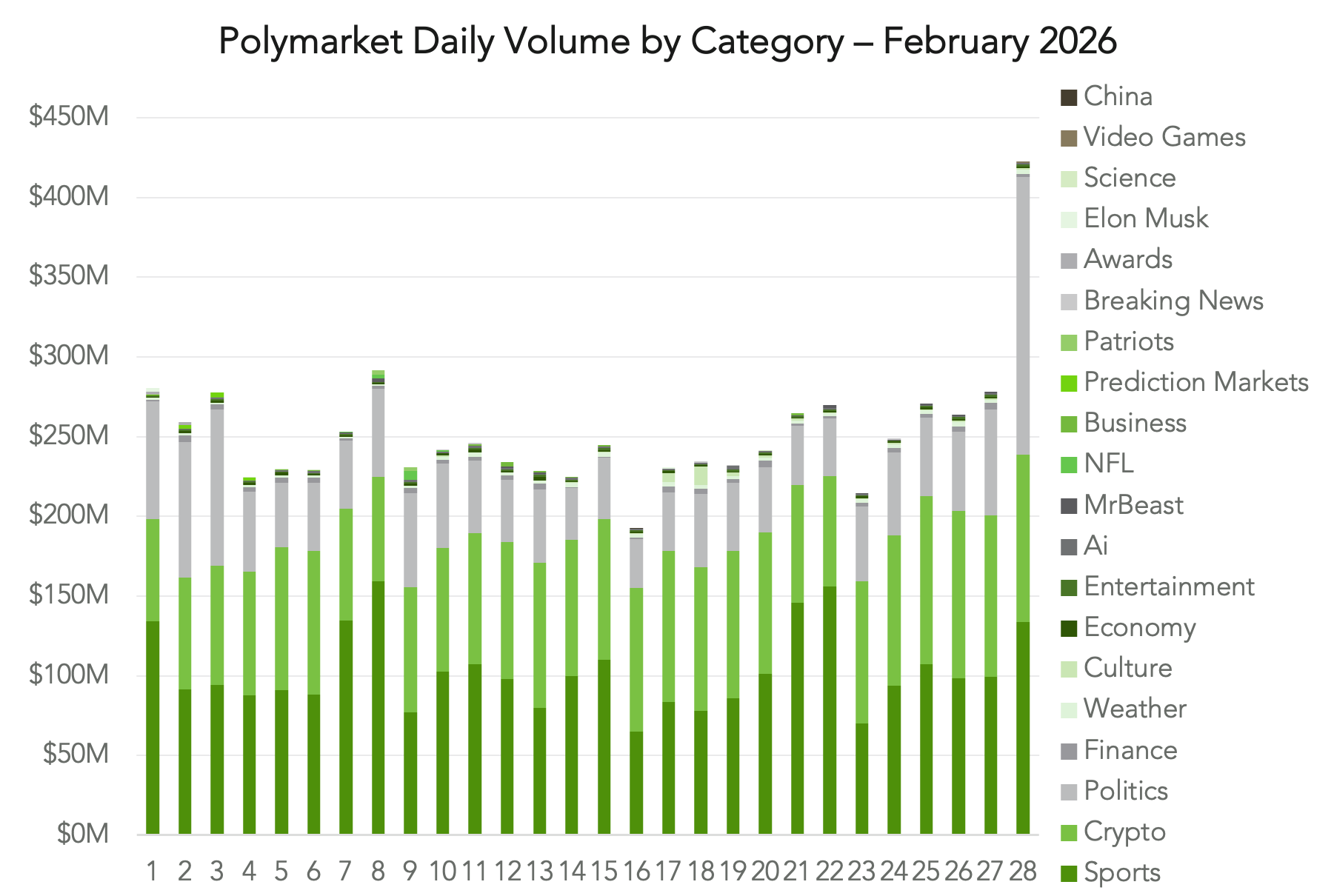

The scale of this expansion has been significant. Monthly prediction market volume across tracked platforms increased from roughly 13x from August 2025 to January 2026, with negative growth for the first time in February (Figure 3). This liquidity is increasingly deployed to price real-world uncertainty. Daily trading on Polymarket during February was dominated by categories such as politics, economics, and breaking news, reflecting how participants use these markets to assess geopolitical and macro risks (Figure 4).

Markets tied to developments in the Middle East, including contracts speculating on the removal of Iran’s leadership, drew significant activity as the month closed. Some traders generated large profits, raising concerns about whether participants could be trading on privileged information ahead of geopolitical events.

This divergence between crypto-native and regulated platforms has placed prediction markets in a complex regulatory landscape, prompting scrutiny from lawmakers ranging from issues around sports betting to insider trading. While Kalshi functions as a CFTC-regulated derivatives exchange, crypto-native platforms such as Polymarket operate on blockchain rails outside traditional regulatory oversight. Questions around market integrity, insider information, and the classification of event contracts remain unresolved, highlighting the unsettled legal environment surrounding this rapidly expanding market.

Despite these debates, prediction markets are increasingly functioning as a new layer of probabilistic price discovery, allowing participants to trade geopolitical and macro uncertainty often before those risks are fully reflected in traditional financial markets.

Prediction Markets Price Real-World Uncertainty

Figure 3

Source: “Kalshi, Polymarket Combine for $17.9B February Volume as Polymarket Closes Gap.” Published by DeFi Rate, March 2, 2026.

Figure 4

Source: https://dune.com/filarm/polymarket-activity; data retrieved March 6, 2026.

Even as digital asset markets experienced heightened volatility in February, conversations among institutional investors suggested that long-term engagement with the asset class continues to deepen.

The final week of February brought thousands of allocators, hedge fund managers, and service providers to Miami for iConnections Global Alts, one of the largest gatherings of alternative investment professionals. While the conference spans the broader alternatives industry, digital assets were a prominent topic across panels and private meetings, reflecting a clear shift from early-stage curiosity toward more deliberate capital allocation discussions.

What stood out this year, as noted by Samara Alpha CIO Adil Abdulali, was the strong presence of traditional finance investors actively evaluating the space. In prior cycles, conversations often centered on whether institutions would participate in digital assets. This year, the discussion had largely moved to how to allocate and which strategies may offer the most compelling risk-adjusted opportunities.

Interest spanned multiple segments of the ecosystem, including DeFi yield strategies, directional and momentum trading, and relative-value opportunities. Several allocators also expressed curiosity around bitcoin-denominated investment structures, which some view as a more natural framework for evaluating performance within the digital asset ecosystem.

This shift reflects a broader evolution in institutional thinking. The market is no longer operating on the assumption that broad beta will do the work. That phase appears to be ending, replaced by more deliberate capital allocation as investors prepare for an environment characterized by greater dispersion between sectors, wider trading ranges, and increased sensitivity to macro liquidity conditions.

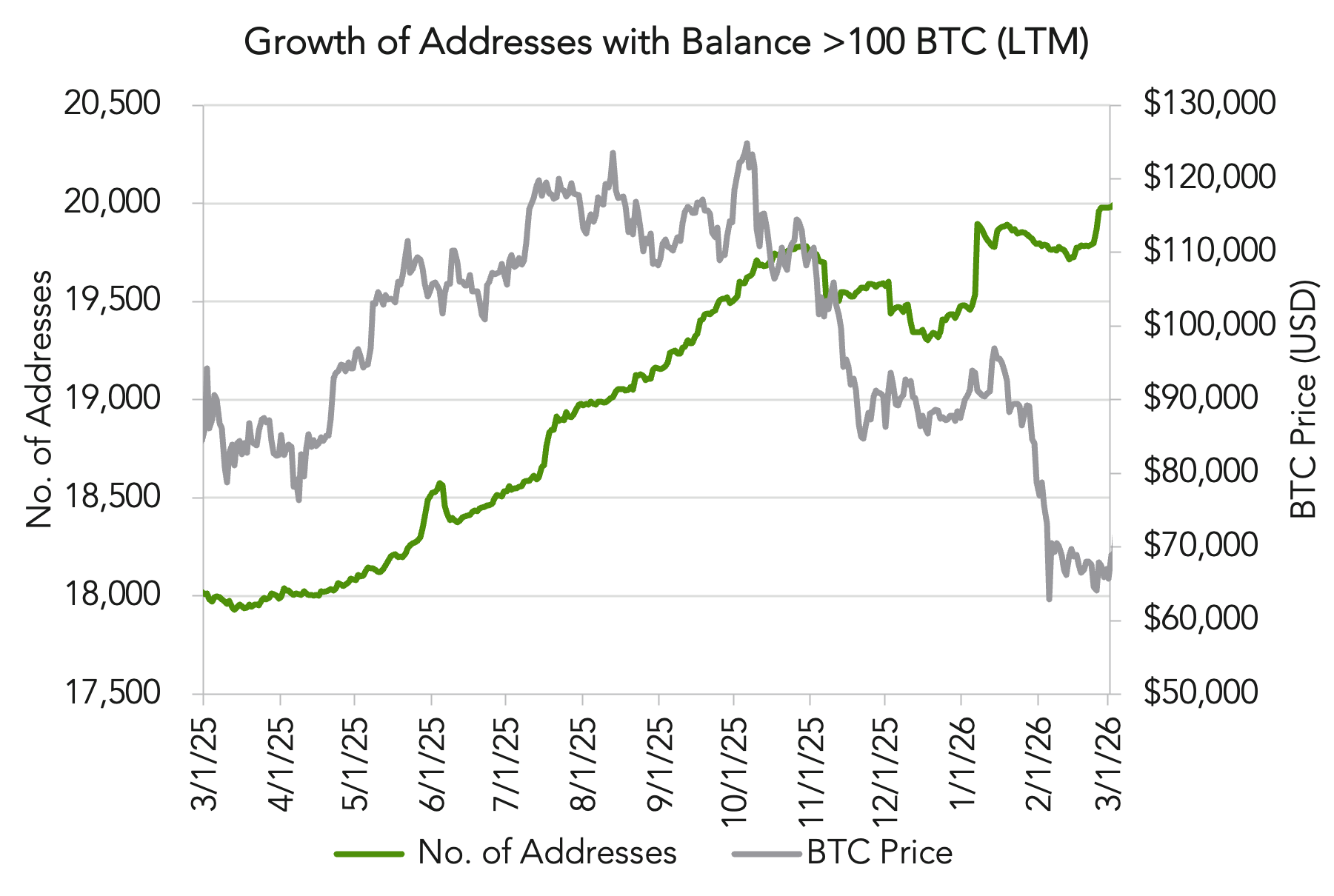

The contrast with retail sentiment during the recent market drawdown was notable. While retail participation often weakens during periods of price volatility, institutional investors appeared largely unfazed, reflecting longer investment horizons and a growing familiarity with the asset class. On-chain data reinforces this dynamic: the number of addresses holding more than 100 BTC has continued to rise over the past year even as prices retraced (Figure 5).

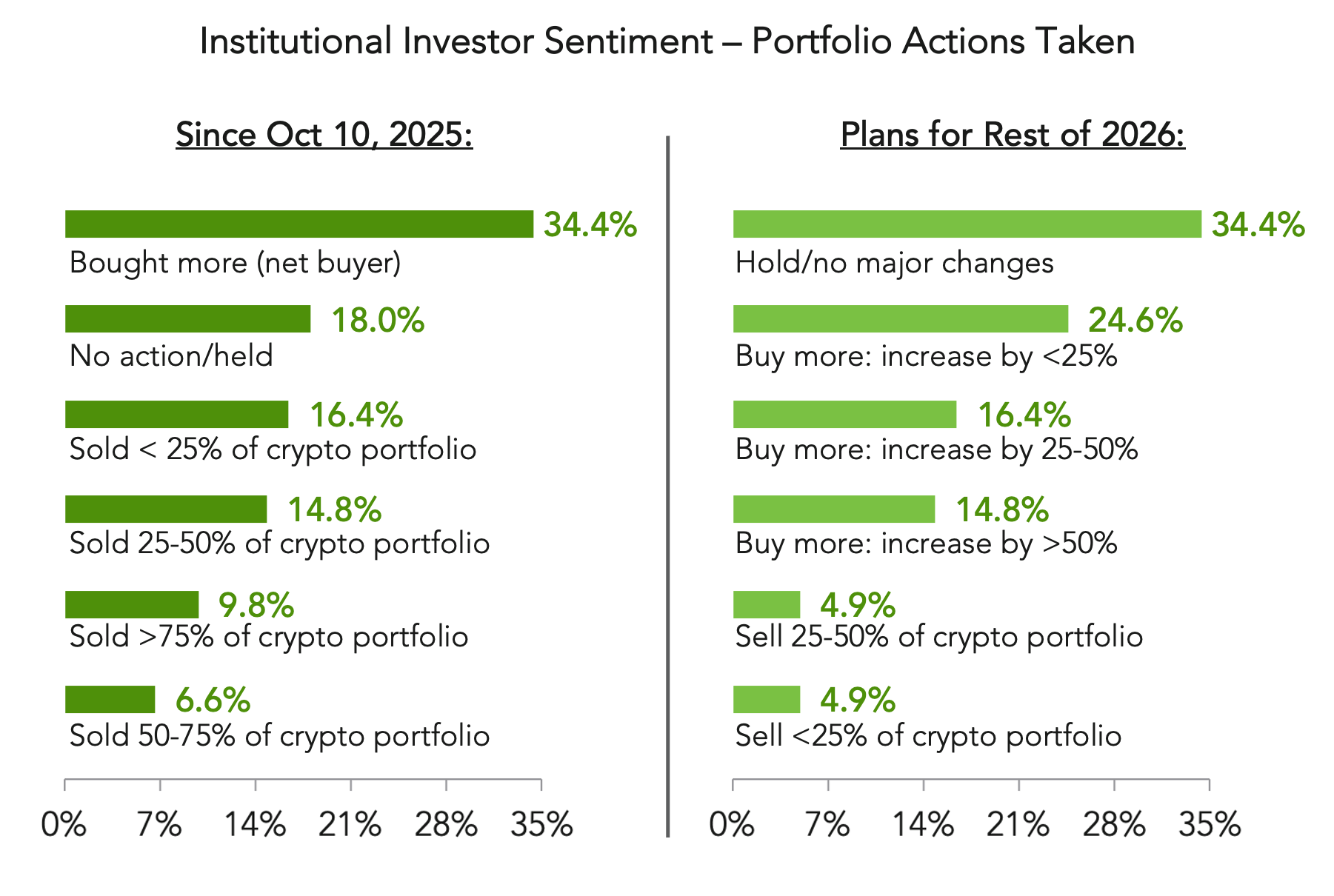

Institutional positioning data points to a similar conclusion. As illustrated in Figure 6, while many investors believe the most aggressive phase of the cycle may have passed, 55.8% still intend to increase digital asset exposure in 2026. Institutions are not questioning the asset class itself; they are reassessing where to deploy capital within it.

Developments during and immediately after the conference further underscored this institutional momentum. While the event was underway, Citigroup announced plans to expand its bitcoin-related capabilities within its financial infrastructure, responding to growing demand from institutional clients seeking access through traditional banking platforms. Days later, Kraken’s banking subsidiary received approval for a Federal Reserve master account, granting direct access to the Fed’s payment rails through Fedwire.

Taken together, the signals point to a market entering a more disciplined phase. The easy upside of the cycle may have passed, but institutional capital is not retreating. Instead, it is repositioning — emphasizing strategy selection, capital efficiency, and balance sheet strength as the next stage of the market unfolds.

Institutions Stay the Crypto Course

Figure 5

Figure 6

Source: “Crypto Sentiment Institutional Investors Survey — Q1 2026.” MV Global and Crypto Funds Watch research published February 24, 2026. Responses from 61 institutional crypto investors, including senior executives at leading crypto hedge funds, venture capital managers, multi-strategy firms, and professional allocators, collected February 9-18.